Example: Sell 1 put; buy 1 put at higher strike

Market Outlook: Bearish

Risk: Limited

Reward: Limited

Increase in Volatility: Helps or hurts depending on strikes chosen

Time Erosion: Helps or hurts depending on strikes chosen

Break even: Long put strike minus net premium paid

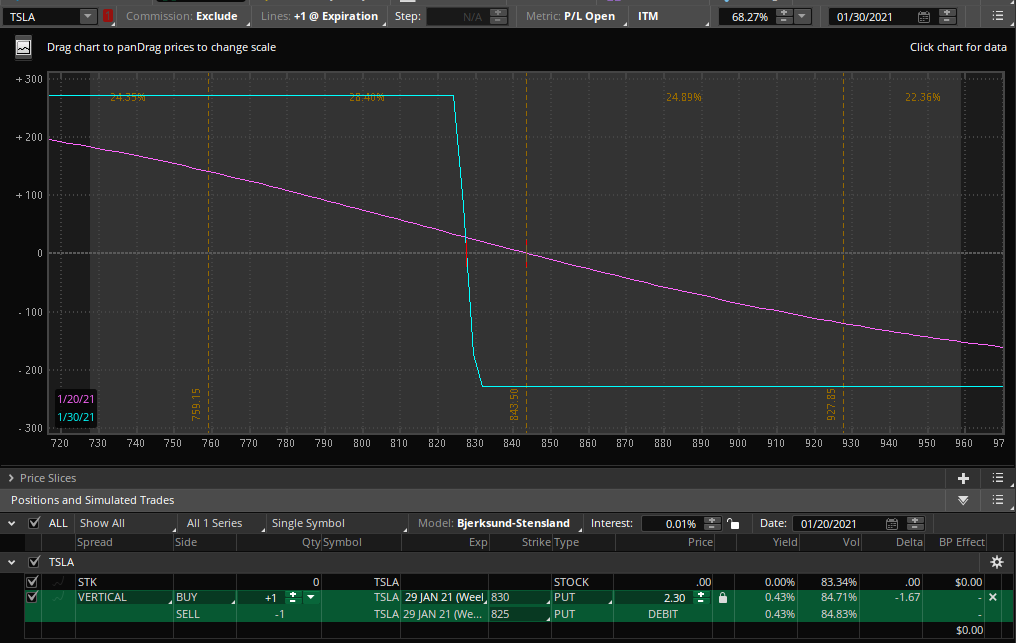

A bear put spread consists of buying one put and selling another put, at a lower strike, to offset part of the upfront cost.

Description

A bear put spread is a type of vertical spread. It consists of buying one put in hopes of profiting from a decline in the underlying stock, and writing another put with the same expiration, but with a lower strike price, as a way to offset some of the cost. Because of the way the strike prices are selected, this strategy requires a net cash outlay (net debit) at the outset.

Assuming the stock moves down toward the lower strike price, the bear put spread works a lot like its long put component would as a standalone strategy. However, in contrast to a plain long put, the possibility of greater profits stops there. This is part of the tradeoff; the short put premium mitigates the cost of the strategy but also sets a ceiling on the profits.

A different pair of strike price choices might work, provided that the short put strike is below the long put strike. The choice is a matter of balancing tradeoffs and keeping to a realistic forecast.

EXAMPLE

- Long 1 XYZ 60 put

- Short 1 XYZ 55 put

MAXIMUM GAIN

- High strike – low strike – net premium paid

MAXIMUM LOSS

- Net premium paid

The lower the short put strike, the higher the potential maximum profit; but that benefit has to be weighed against the disadvantage: a smaller amount of premium received.

It is interesting to compare this strategy to the bear call spread. The profit/loss payoff profiles are exactly the same, once adjusted for the net cost to carry. The chief difference is the timing of the cash flows. The bear put spread requires a known initial outlay for an unknown eventual return; the bear call spread produces a known initial cash inflow in exchange for a possible outlay later on.

Outlook

Looking for a steady or declining stock price during the term of the options.

While the longer-term outlook is secondary, there is an argument for considering another alternative if the investor is bearish on the stock’s future. It would take careful pinpointing to forecast when an expected rally would end and the eventual decline would start.

Summary

A bear put spread consists of buying one put and selling another put, at a lower strike, to offset part of the upfront cost. The spread generally profits if the stock price moves lower. The potential profit is limited, but so is the risk should the stock unexpectedly rally.

Motivation

Profit from a near-term decline in the underlying stock.

Variations

A vertical put spread can be a bullish or bearish strategy, depending on how the strike prices are selected for the long and short positions. See bull put spread for the bullish counterpart.

Max Loss

The maximum loss is limited. The worst that can happen at expiration is for the stock to be above the higher (long put) strike price. In that case, both put options expire worthless, and the loss incurred is simply the initial outlay for the position (the debit).

Max Gain

The maximum gain is limited. The best that can happen is for the stock price to be below the lower strike at expiration. The upper limit of profitability is reached at that point, even if the stock were to decline further. Assuming the stock price is below both strike prices at expiration, the investor would exercise the long put component and presumably be assigned on the short put. So, the stock is sold at the higher (long put strike) price and simultaneously bought at the lower (short put strike) price. The maximum profit then is the difference between the two strike prices, less the initial outlay (the debit) paid to establish the spread.

Profit/Loss

Both the potential profit and loss for this strategy are very limited and very well defined. The net premium paid at the outset establishes the maximum risk, and the short put strike price sets the upper boundary, beyond which further stock price erosion won’t improve the profitability. The maximum profit is limited to the difference between the strike prices, less the debit paid to put on the position.

The investor can alter the profit/loss boundaries by selecting different strike prices. However, each choice represents the classic risk/reward tradeoff: greater opportunities and risk, versus more limited opportunities and risk.

Breakeven

This strategy breaks even if, at expiration, the stock price is below the upper strike by the amount of the initial outlay (the debit). In that case, the short put would expire worthless, and the long put’s intrinsic value would equal the debit.

Breakeven = long put strike – net debit paid

Volatility

Slight, all other things being equal. Since the strategy involves being short one put and long another with the same expiration, the effects of volatility shifts on the two contracts may offset each other to a large degree.

Note, however, that the stock price can move in such a way that a volatility change would affect one price more than the other.

Time Decay

The passage of time hurts the position, though not quite as much as it does an plain long put position. Since the strategy involves being long one put and short another with the same expiration, the effects of time decay on the two contracts may offset each other to a large degree.

Regardless of the theoretical impact of time erosion on the two contracts, it makes sense to think the passage of time would be somewhat of a negative. This strategy requires a non-refundable initial investment. If there are to be any returns on the investment, they must be realized by expiration. As expiration nears, so does the deadline for achieving any profits.

Assignment Risk

Yes. Early assignment, while possible at any time, generally occurs only when a put option goes deep into-the-money. Be warned, however, that using the long put to cover the short put assignment will require financing a long stock position for one business day.

And be aware, any situation where a stock is involved in a restructuring or capitalization event, such as for example a merger, takeover, spin-off or special dividend, could completely upset typical expectations regarding early exercise of options on the stock.

Expiration Risk

Yes. If held into expiration, this strategy entails added risk. The investor cannot know for sure until the following Monday whether or not the short put was assigned. The problem is most acute if the stock is trading just below, at or just above the short put strike. Guessing wrong either way could be costly.

Assume that on Friday afternoon the long put is deep-in-the-money, and that the short put is roughly at-the-money. Exercise (stock sale) is certain, but assignment (stock purchase) isn’t. If the investor guesses wrong, the new position next week will be wrong, too. Say, assignment is anticipated but fails to occur; the investor won’t discover the unintended net short stock position until the following Monday, and is subject to an adverse rise in the stock over the weekend. Now assume the investor bet against assignment and bought the stock in the market to liquidate the position. Come Monday, if assignment occurred after all, the investor has bought the same shares twice, for a net long stock position and exposure to a decline in the stock price.

Two ways to prepare: close the spread out early or be prepared for either outcome on Monday. Either way, it’s important to monitor the stock, especially over the last day of trading.

Credit to https://www.optionseducation.org and theocc.com for the educational description.