Example: Buy put

Market Outlook: Bearish

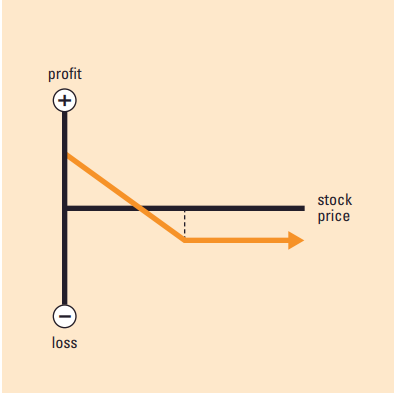

Risk: Limited

Reward: Limited, but substantial

Increase in Volatility: Helps position

Time Erosion: Hurts position

Break Even: Strike price minus premium paid

This strategy consists of buying puts as a means to profit if the stock price moves lower.

Description

The investor buys a put contract that is compatible with the expected timing and size of a downturn. Although a put usually doesn’t appreciate $1 for every $1 that the stock declines, the percentage gains can be significant.

Exercising a put would result in the sale of the underlying stock. These comments focus on long puts as a standalone strategy, so exercising the option would result in a short stock position, something not all individuals would choose as a goal. The plan here is to resell the put at a profit before expiration. The investor is hoping for a dramatic downturn; the sooner, the better.

Timing is of the essence. Some put holders set price targets or re-evaluation dates; others ‘play it by ear.’ Either way, all value must be realized before the put expires. If the expected results have not materialized as expiration draws near, a careful investor is ready to re-evaluate.

EXAMPLE

- Long 1 XYZ 60 put

MAXIMUM GAIN

- Strike price – premium paid

MAXIMUM LOSS

- Premium paid

If the put holder is willing to forfeit 100% of the premium paid and is convinced a decline is imminent, one choice is to wait until the last trading day. If the stock falls, the put might generate a nice profit after all. However, if a quick correction looks unlikely, it might make sense to sell the put while it still has some time value. A timely decision might recover part or even all of the investment.

Outlook

The investor is looking for a sharp decline in the stock’s price during the life of the option.

This strategy is compatible with a variety of long-term forecasts for the underlying stock, from very bearish to neutral. However, if the investor is firmly bullish on the underlying stock in the long run, other strategy alternatives might be more suitable.

Summary

This strategy consists of buying puts as a means to profit if the stock price moves lower. It is a candidate for bearish investors who want to participate in an anticipated downturn, but without the risk and inconveniences of selling the stock short.

The time horizon is limited to the life of the option.

Motivation

A put buyer has the opportunity to profit from a fall in the stock’s price, without risking an unlimited amount of capital, as a short stock seller does. What’s more, the leverage involved in a long put strategy can generate attractive percentage returns if the forecast is right.

Another common use for puts is hedging a long stock position. It is described separately under protective put.

Variations

These remarks are targeted toward the investor who buys puts as a standalone strategy. See the discussion on protective puts for a discussion on using long puts as a way to hedge or exit a long stock position.

Max Loss

The maximum loss is limited. The worst that can happen is for the stock price to be above the strike price at expiration with the put owner still holding the position. The put option expires worthless and the loss is the price paid for the put.

Max Gain

The profit potential is limited but substantial. The best that can happen is for the stock to become worthless. In that case, the investor can theoretically do one of two things: sell the put for its intrinsic value or exercise the put to sell the underlying stock at the strike price and simultaneously buy the equivalent amount of shares in the market at, theoretically, zero cost. The investor’s profit would be the difference between the strike price and zero, less the premium paid, commissions and fees.

Profit/Loss

The profit potential is significant, and the losses are limited to the premium paid.

Although a put option is unlikely to appreciate $1 for every $1 that the stock declines during most of the option’s life, the gains could be substantial if the stock falls sharply. Generally speaking, the earlier and more dramatic the drop in the stock’s value, the better for the long put strategy. Given that the premium investment can be small relative to the stock value it represents, the potential percentage gains and losses can be large, with the caveat that they must be realized by the time the option expires.

All other things being equal, an option typically loses time value premium with every passing day, and the rate of time value erosion tends to accelerate. That means the long put holder may not be able to re-sell the option at a profit unless at least one major pricing factor changes favorably. The most obvious would be an decline in the underlying stock’s price. A rise in volatility could also help significantly by boosting the put’s time value.

An option holder cannot lose more than the initial price paid for the option.

Breakeven

At expiration, the strategy breaks even if the stock price equals the strike price minus the cost of the option. Any stock price below that level produces a net profit. In other words:

Breakeven = strike – premium

Volatility

An increase in implied volatility would have a positive impact on this strategy, all other things being equal. Volatility tends to boost the value of any long option strategy, because it indicates a greater mathematical probability that the stock will move enough to give the option intrinsic value (or add to its current intrinsic value) by expiration day.

By the same logic, a decline in volatility has a tendency to lower the long put strategy’s value, regardless of the overall stock price trend.

Time Decay

As with most long option strategies, the passage of time has a negative impact, all other things being equal. As time remaining until expiration disappears, the statistical chances of achieving further gains shrink. That tends to be reflected in eroding time premiums, which put downward pressure on the put’s market value.

Once time value disappears, all that remains is intrinsic value. For in-the-money options, that is the difference between the going stock price and the strike price. For at-the-money and out-of-the-money options, intrinsic value is zero.

Assignment Risk

None. The investor is in control.

Expiration Risk

Slight. If the option is in-the-money at expiration, it may be exercised on your behalf by your brokerage firm. Since this investor did not own the underlying stock, an unexpected exercise could require urgent measures to find the stock for delivery at settlement. A short stock position might be a problematic outcome for an individual investor.

Every investor carrying a long option position into expiration is urged to verify all related procedures with their brokerage firm: automatic exercise minimums, exercise notification deadlines, etc.

Comments

All option investors have reason to monitor the underlying stock and keep track of dividends. This applies to long put investors, too.

On an ex-dividend date, the amount of the dividend is deducted from the value of the underlying stock. Assuming nothing else has changed, a lower stock value typically boosts the put option’s value. The effect is foreseeable and usually gets factored more gradually, but dividend dates could nevertheless be one consideration in deciding when it might be optimal to close out the put position.

Credit to https://www.optionseducation.org and theocc.com for the educational description.